SIBONISO NXUMALO | Investors, beware the disappointment of great expectations

The ability to discern if expectations are realistic or veer into overly optimistic territory is a skill that separates successful investors from the crowd

20 March 2024 - 08:25

Picture: OMIG

About the author: Siboniso Nxumalo is chief investment officer at Old Mutual Investment Group. Picture: OMIG

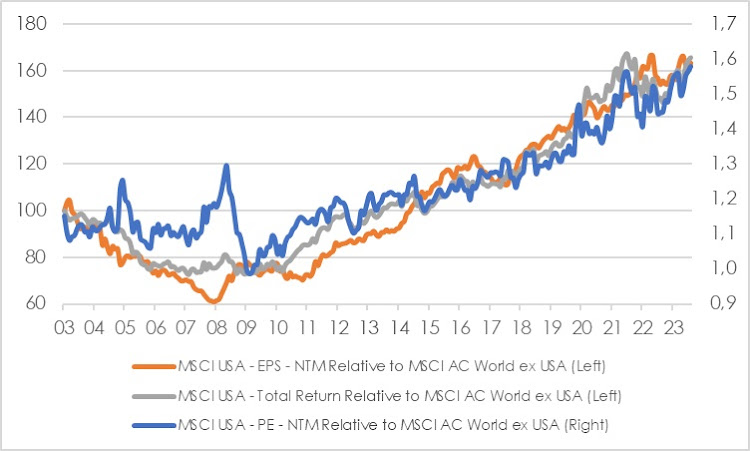

US return vs rest of the world. Source: MSCI, Factset

US return vs rest of the world. Source: MSCI, Factset

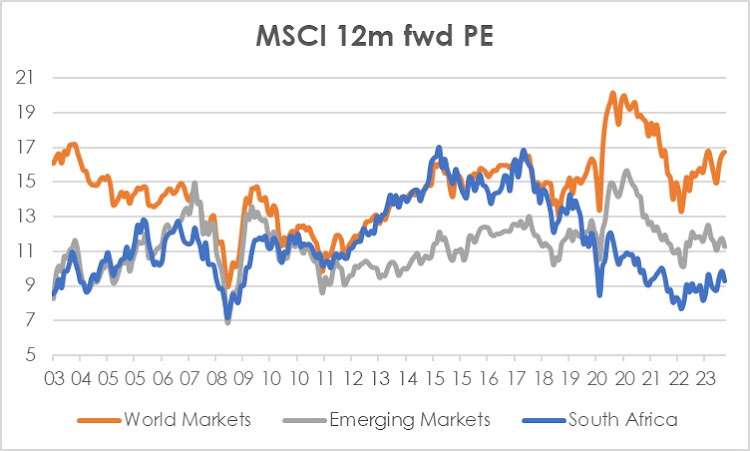

MSCI 12m forward PE. Source: MSCI, Factset